Students can Download Computer Applications Chapter 16 Electronic Payment Systems Questions and Answers, Notes Pdf, Samacheer Kalvi 12th Computer Applications Book Solutions Guide Pdf helps you to revise the complete Tamilnadu State Board New Syllabus and score more marks in your examinations.

Tamilnadu Samacheer Kalvi 12th Computer Applications Solutions Chapter 16 Electronic Payment Systems

Samacheer Kalvi 12th Computer Applications Electronic Payment Systems Text Book Back Questions and Answers

PART – I

I. Choose The Correct Answer

Question 1.

Based on the monetary value e payment system can be classified into

(a) Mirco and Macro

(b) Micro and Nano

(c) Maximum and Minimum

(d) Maximum and Macro

Answer:

(a) Mirco and Macro

![]()

Question 2.

Which of the following is not a category of micro payment?

(a) Buying a movie ticket

(b) Subscription to e journals

(c) Buying a laptop

(d) Paying for smart phone app

Answer:

(c) Buying a laptop

Question 3.

Assertion (A): Micro electronic payment systems support higher value payments.

Reason (R): Expensive cryptographic operations are included in macro payments

(a) Both (A) and (R) are correct and (R) is the correct explanation of (A)

(b) Both (A) and (R) are correct, but (R) is not the correct explanation of (A)

(c) (A) is true and (R) is false

(d) (A) is false and (R) is true

Answer:

(d) (A) is false and (R) is true

![]()

Question 4.

Which of the following is correctly matched

(a) Credit Cards – pay before

(b) Debit Cards – pay now

(c) Stored Value Card – pay later

(d) Smart card – pay anytime

Answer:

(b) Debit Cards – pay now

Question 5.

ECS stands for

(a) Electronic Clearing Services

(b) Electronic Cloning Serivces

(c) Electronic Clearing Station

(d) Electornic Cloning Station

Answer:

(a) Electronic Clearing Services

![]()

Question 6.

Which of the following is not a Altcoin

(a) Litecoin

(b) Namecoin

(c) Ethereum

(d) Bitcoin

Answer:

(c) Ethereum

Question 7.

Which of the following is true about Virtual payment address (VPA)

(a) Customers can use their e-mail id as VPA

(b) VPA does not includes numbers

(c) VPA is a unique ID

(d) Multiple bank accounts cannot have single VPA

Answer:

(d) Multiple bank accounts cannot have single VPA

![]()

Question 8.

Pick the odd one in the credit card transaction

(a) card holder

(b) merchant

(c) marketing manager

(d) acquirer

Answer:

(c) marketing manager

Question 9.

Which of the following is true about debit card

(i) debit cards cannot be used in ATMs

(ii) debit cards cannot be used in online transactions

(iii) debit cards do not need bank accounts

(iv) debit cards and credit cards are identical in physical properties

(a) (i), (ii), (iii)

(b) (ii), (iii), (iv)

(c) (iii) alone

(d) (iv) alone

Answer:

(d) (iv) alone

![]()

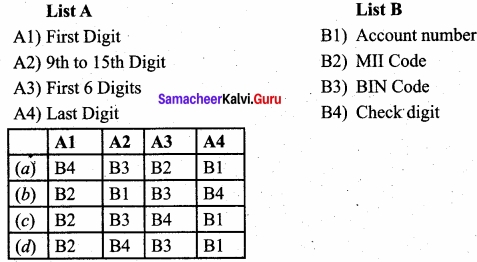

Question 10.

Match the following

Answer:

(b) A1-B2, A2-B1, A3-B3, A4-B4

II. Short Answers

Question 1.

Define electronic payment system?

Answer:

The term electronic payment refers to a payment made from one bank account to another bank account using electronic methods forgoing the direct intervention of bank employees.

![]()

Question 2.

Distinguish micro electronic payment and macro electronic payment?

Answer:

Micro Electronic Payment System:

- Payments of small system amount

- Less Security

- Eg. Subscriptions of online games

Macro Electronic Payment System:

- Payments of higher value

- Highly Secured

- Electronic account transfer

![]()

Question 3.

List the types of micro electronic payments based on its algorithm?

Answer:

- Hash chain based micro electronic payment systems.

- Hash collisions and hash sequences based micro electronic payment systems.

- Shared secrete keys based micro electronic payment systems.

- Probability based micro electronic payment systems.

Question 4.

Explain the concept of e-wallet?

Answer:

Electronic wallets (e-wallets) or electronic purses allow users to make electronic transactions quickly and securely over the Internet through smartphones or computers.

![]()

Question 5.

What is a fork in cryptocurrency?

Answer:

Many cryptocurrencies operate on the basis of the same source code, in which the authors make only a few minor changes in parameters like time, date, distribution of blocks, number of coins, etc. These currencies are called as fork. In fork, both cryptocurrencies can share a common transaction history in block chain until the split.

PART – III

III. Explain in Brief Answers

Question 1.

Define micro electronic payment and its role in E-Commerce?

Answer:

- It is an on-line payment system designed to allow efficient and frequent payments of small amounts.

- In order to keep transaction costs very low, the communication and computational costs are minimized here.

- The security of micro electronic payment systems is comparatively low

- The majority of micro electronic payment systems were designed to pay for simple goods on the Internet, e.g., subscriptions of online games, read journals, listen to a song or watch a movie online etc.

![]()

Question 2.

Compare and contrast the credit card and debit card?

Answer:

Credit Card:

A credit card is different from a debit card where the credit card issuer lends money to customer instead of deducting it from customer’s bank account instantly.

Debit Card:

Credit card is an electronic payment system normally used for retail transactions. A credit card enables the bearer to buy goods or services from a vendor, based on the cardholder’s promise to the card issuer to payback the value later with an agreed interest.

Question 3.

Explain briefly Anatomy of a credit card?

Answer:

Publisher:

Emblem of the issuing bank

Credit card number:

The modem credit card number has 16-digit unique identification number.

![]()

Question 4.

Briefly explain the stored value card and its types?

Answer:

(i) Closed loop (single purpose):

In closed loop cards, money is metaphorically stored on the card in the form of binary- coded data. e.g. chennai metro rail travel card.

(ii) Open loop (multipurpose):

It is also called as prepaid-debit cards, e.g. Visa gift cards.

![]()

Question 5.

Write a note on mining in cryptocurrency?

Answer:

Mining:

The cryptocurrency units are created by the solution of cryptographic tasks called mining. The miners not only generate new monetary units, but also initiate new transactions to the blockchain. As a reward, they will receive new Bitcoins.

PART – IV

IV. Explain in detail

Question 1.

What is credit card? Explain the key players of a credit card payment system and bring out the merits of it?

Answer:

Credit Card:

Credit card is an electronic payment system normally used for retail transactions. A credit card enables the bearer to buy goods or services from a vendor, based on the cardholder’s promise to the card issuer to payback the value later with an agreed interest. Every credit card account has a purchase limit set by the issuing bank or the firm. A credit card is different from a debit card where the credit card issuer lends money to customer instead of deducting it from customer’s bank account instantly.

The term credit card was first mentioned in 1887 in the sci-fi novel “Looking Backward” by Edward Bellamy. The modem credit cards concept was bom in the U.S.A, in the 1920s, when private companies began to issue cards to enable their customers to purchase goods on credit within their own premises.

Advantages of credit card:

- Most credit cards are accepted worldwide.

- It is not necessary to pay physical money at the time of purchase. The customer gets an extra period to pay the purchase.

- Depending on the card, there is no need to pay annuity.

- Allows purchases over the Internet in installments.

- Some issuers allows “round up” the purchase price and pay the difference in cash to make the transactions easy.

Key players in operations of credit card:

1. Bearer:

The holder of the credit card account who is responsible for payment of invoices in full (transactor) or a portion of the balance (revolver) the rest accrues interest and carried forward.

2. Merchant:

Storekeeper or vendor who sell or providing service, receiving payment made by its customers through the credit card.

3. Acquirer:

Merchant’s bank that is responsible for receiving payment on behalf of merchant send authorization requests to the issuing bank through the appropriate channels.

4. Credit Card Network:

It acts as the intermediate between the banks. The Company responsible for communicating the transaction between the acquirer and the credit card issuer. These entities operate

the networks that process credit card payments worldwide and levy interchange fees. E.g. Visa, MasterCard, Rupay

5. Issuer:

Bearer’s bank, that issue the credit card, set limit of purchases, decides the approval – of transactions, issue invoices for payment, charges the holders in case of default and offer card-linked products such as insurance, additional cards and rewards plan.

![]()

Question 2.

Briefly explain Electronic Account transfer and its types?

Answer:

With the advent of computers, network technologies and electronic communications a large number of alternative electronic payment systems have emerged. These include ECS (Electronic Clearing Services), EFT (Electronic funds transfers), Real Time Gross Settlement system (RTGS) etc.

1. Electronic Clearing Services (ECS):

Electronic Clearing Service can be defined as repeated transfer of funds from one bank account to multiple bank accounts or vice versa using computer and Internet technology. Advantages of this system are bulk payments, guaranteed payments and no need to remember payment dates. ECS can be used for both credit and debit purposes i.e. for making bulk payments or bulk collection of amounts.

2. ECS credit:

ECS credit is used for making bulk payment of amounts. In this mode, a single account is debited and multiple accounts are credited. This type of transactions are Push transactions. Example: if a company has to pay salary to its 100 employees it can use ECS credit system than crediting every employees’ account separately.

3. ECS debit:

ECS debit is an inverse of ECS credit. It is used for bulk collection of amounts. In this mode, multiple accounts are debited and then a single account is credited. This type of transactions are Pull transactions. Example: The insurance premium of bulk number of customers

4. Electronic Funds Transfer:

Electronic Funds Transfer (EFT) is the “electronic transfer” of money over an online network. The amount sent from the sender’s bank branch is credited to the receiver’s bank branch on the same day in batches.

5. Real Time Gross Settlement:

Real Time Gross Settlement system (RTGS) is a payment system particularly used for the settlement of transactions between financial institutions, especially banks.

Real-time gross settlement transactions are:

1. Unconditional – the beneficiary will receive funds regardless of whether he 242 fulfills his obligations to the buyer or whether he would deliver the goods or perform a service of a quality consistent with the order.

2. Irrevocable – a correctly processed transaction cannot be reversed and its money cannot get refunded (the so-called settlement finality).

![]()

Question 3.

Write a note on

(a) Internet banking

(b) Mobile banking

(a) Internet banking:

Internet banking is a collective term for E-banking, online banking, virtual banking (operates only on the Internet with no physical branches), direct banks, web banking and remote banking. Internet banking allows customers of a financial institution to conduct various financial transactions on a secure website operated by the banking institutions. This is a very fast and convenient way of performing any banking transactions.

It enables customers of a bank to conduct a wide range of financial transactions through its website. In fact, it is like a branch exclusively operating of an individual customer. The online banking system will typically connect to the core banking system operated by customers themselves (Self-service banking).

Advantages:

- The advantages of Internet banking are that the payments are made at the convenience of the account holder and are secured by user name and password, i.e. with Internet access it can be used from anywhere in the world and at any time.

- Any standard browser (e.g. Google Chrome) is adequate. Internet banking does not need .installing any additional software.

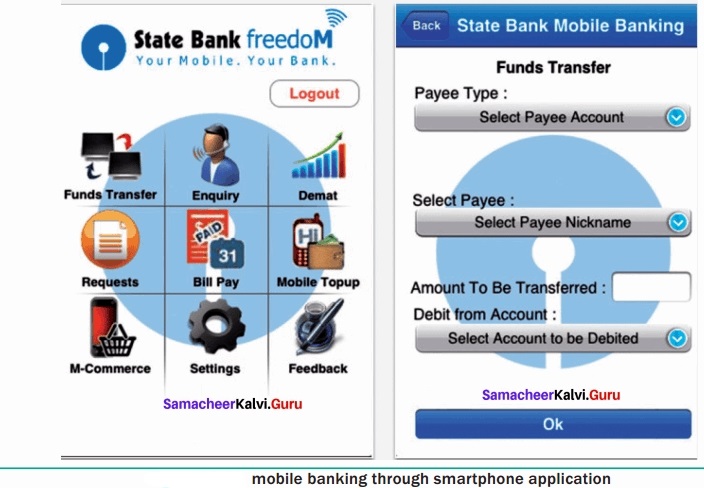

(b) Mobile banking:

Mobile banking is another form of net banking. The term mobile banking (also called m-banking) refers to the services provided by the bank to the customer to conduct banking transactions with the aid of mobile phones. These transactions include balance checking, account transfers, payments, purchases, etc.

Transactions can be done at any time and anywhere. The WAP protocol installed on a mobile phone qualifies the device through an appropriate application for mobile session establishment with the bank’s website. In this way, the user has the option of permanent control over the account and remote management of his own finances. Mobile Banking operations can be implemented in the following ways:

- Contacting the call center.

- Automatic IVR telephone service.

- Using a mobile phone via SMS.

- WAP technology.

- Using smartphone applications.

Question 4.

What is cryptocurrency? Explain the same?

Answer:

Cryptocurrency:

- People have always valued unique and irreplaceable things. A unique thing always has a demand and acclaims a price.

- A cryptocurrency is a unique virtual (digital) asset designed to work as a medium of exchange using cryptographic algorithm.

- This algorithm secures the transactions by recording it in blockchain and controls the creation of additional units of the currency.

- Cryptocurrency is also called as cryptocoins, e-cash, alternative currencies or virtual currencies and are classified as a subset of digital currencies.

- Cryptocurrency can be defined as distributed accounting system based on cryptography, storing information about the state of ownership in conventional units.

- The state of ownership of a cryptocurrency is related to individual system blocks called “portfolios”.

- Only the holder of the corresponding private key would have control over a given portfolio and it is impossible to issue the same unit twice.

- The function of cryptocurrency is based on technologies such as Mining, Blockchain, Directed Acyclic Graph, Distributed register (ledger), etc. The information about the . transaction is usually not encrypted and is available in clear text.

Bitcoin:

Bitcoin is the most popular and the first decentralized cryptocurrency. Bitcoin is the most popular cryptocurrency, but there are many other cryptocurrencies, which are referred to as “altcoins”.

Altcoins:

- Altcoins is the collective name for all cryptocurrencies that appeared after Bitcoin. The early Altcoins Litecoin and Namecoin appeared in 2011.

- From 2014, the 2nd generation of cryptocurrency appeared, such as Monero, Ethereum and Nxt. These crypto-coins have advanced features such as hidden addresses and smart contracts.

- In terms of trade, the creation of cryptocurrencies may be related to the ICO (Initial Coin Offer) procedure.

Block chain:

- Block chains are an open distributed book that records transactions of cryptocurrencies between any two parties in an efficient and verifiable manner.

- It is a continuously growing list of records, called blocks, which are linked to each other and protected using encryption algorithm.

Each block typically contains a hash pointer as a link to a previous block. It records data about every transaction with its date and time. - Once recorded, the data in any given block cannot be altered without the alteration of all subsequent blocks.

![]()

Question 5.

Explain in detail: Unified payments interface?

Answer:

(i) Unified Payments Interface (UPI) is a real-time payment system developed by National Payments Corporation of India (NCPI) to facilitate inter-bank transactions.

(ii) It is simple, secure and instant payment facility. This interface is regulated by the Reserve Bank of India and used for transferring funds instantly between two bank accounts through mobile (platform) devices. http://www. npci.org.in/

(iii) Unlike traditional e-wallets, which take a specified amount of money from user and store it in its own account, UPI withdraws and deposits funds directly from the bank account whenever a transaction is requested.

(iv) It also provides the “peer to peer” collect request which can be scheduled and paid as per requirement and convenience.

(v) UPI is developed on the basis of Immediate Payment Service (IMPS). To initiate a transaction, UPI applications use two types of address – global and local.

- Global address includes bank account numbers and IFSC.

- Local address is a virtual payment address.

(vi) Virtual payment address (VPA) also called as UPI-ID, is a unique ID similar to email id

(e.g. name@bankname) enable us to send and receive money from multiple banks and prepaid payment issuers.

(vii) Bank or the financial institution allows the customer to generate VPA using phone number associated with Aadhaar number and bank account number. VPA replaces bank account details thereby completely hides critical information.

(Viii) The MPIN (Mobile banking Personal Identification number) is required to confirm each payment. UPI allows operating multiple bank accounts in a single mobile application.

(ix) Some UPI application also allows customers to initiate the transaction using only Aadhaar number in absence VPA.

Advantages:

- Immediate money transfers through mobile device round the clock 24 × 7.

- Can use single mobile application for accessing multiple bank accounts.

- Single Click Authentication for transferring of fund.

- It is not required to enter the details such as Card no, Account number, IFSC etc. for every transaction.

- Electronic payments will become much easier without requiring a digital wallet or credit or debit card.

Samacheer Kalvi 12th Computer Applications Electronic Payment Systems Additional Questions and Answers

I. Choose The Best Answer

Question 1.

An electronic payment system is also called as …………………….

(a) liquidation

(b) clearing system

(c) clearing services

(d) all of these

Answer:

(d) all of these

![]()

Question 2.

The electronic payment systems are classified into …………………….. types

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(a) 2

Question 3.

I: Micro Electronic payments are expensive public key cryptography.

II: Security of Micro Electronic Payment is low

(a) t-True, II-False

(b) I-False, II-True

(c) Both I, II are true

(d) Both I, II-False

Answer:

(b) I-False, II-True

Question 4.

Pick the odd one out

(a) read journals

(b) listen to a song

(c) watch a movie online

(d) Internet payment systems

Answer:

(d) Internet payment systems

![]()

Question 5.

…………………….. are plastic cards that enable cashless payments.

Answer:

Payment Cards

Question 6.

How many card based payment systems are available (based on the transaction settlement method)

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(b) 3

![]()

Question 7.

How many micro electronic payments systems are there based on simple cryptographic algorithms?

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(c) 4

Question 8.

……………………… is an electronic payment system normally used for retail transactions.

Answer:

Credit Card

Question 9.

The term credit card was first mentioned in the novel by ……………………..

Answer:

Edward Beltamy

![]()

Question 10.

The term credit card was first mentioned in the sci-fi novel ………………………

(a) Looking Backward

(b) Arrival

(c) Interstellar

(d) Altered States

Answer:

(a) Looking Backward

Question 11.

The term credit cad was first mentioned in the sci-fi normal in the year ………………………

(a) 1997

(b) 1887

(c) 1987

(d) 1897

Answer:

(b) 1887

![]()

Question 12.

The plastic cards was introduced in the year ……………………..

(a) 1957

(b) 1597

(c) 1955

(d) 1855

Answer:

(c) 1955

Question 13.

Who created Diners Club Card?

(i) Frank McNamara

(ii) Ralph Schneider

(iii) Edward Bellamy

(a) (i), (iii)

(b) (ii), (iii)

(c) (i), (ii)

(d) (i), (ii), (iii)

Answer:

(c) (i), (ii)

![]()

Question 14.

The Diners Club Card was created in the year …………………………

(a) 1950

(b) 1955

(c) 1960

(d) 1965

Answer:

(a) 1950

Question 15.

Initially the Diners Club Card was made of ……………………..

(a) paper-cardboard

(b) plastic

(c) wood

(d) metal

Answer:

(a) paper-cardboard

![]()

Question 16.

(I) The Diners Club Card was accepted only in 25 restaurants (initially).

(II) From 1965, the card was made of plastic.

(a) I-True, II-False

(b) I-False, II-True

(c) I, II-both True

(d) I, II-both are false

Answer:

(d) I, II-both are false

Question 17.

How many key players are there in the operation of credit card?

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(d) 5

![]()

Question 18.

The ……………………. is the holder of the credit card account.

Answer:

Bearer

Question 19.

……………………. Network acts as the Intermediate between the banks.

Answer:

Credit Card

Question 20.

The credit card limit, approval of transactions, default charges are issued by

(a) issuer

(b) Merchant

(c) Acquirer

(d) Bearer

Answer:

(a) issuer

![]()

Question 21.

Match the following (description of payment cards)

(i) width – 1.2.88 mm – 3.48 mm

(ii) height – 2. 53.98 mm

(iii) radius – 3. 85.60 mm

(iv) thickness – 4.0.76 mm

(a) (i)-3, (ii)-2, (iii)-1, (iv)-4

(b) (i)-1, (ii)-2, (iii)-3, (iv)-4

(c) (i)-4, (ii)-2, (iii)-1, (iv)-3

(d) (i)-2, (ii)- 1, (iii)-4, (iv)-3

Answer:

(a) (i)-3, (ii)-2, (iii)-1, (iv)-4

Question 22.

The credit card number has ……………………. digit unique identification number

(a) 8

(b) 16

(c) 15

(d) 20

Answer:

(b) 16

Question 27.

EMV means ………………………

Answer:

europay, Mastercard, Visa

![]()

Question 28.

EMV is categorized into ………………………

Answer:

chip and signature, chip and PIN

Question 29.

How many curved lines are there in RFID symbol?

(a) 4

(b) 8

(c) 12

(d) 16

Answer:

(a) 4

Question 30.

……………………. is Ipdian domestic open loop card.

Answer:

Rupay

![]()

Question 31.

Rupay was launched in the year

(a) 2001

(b) 2003

(c) 2009

(d) 2012

Answer:

(d) 2012

Question 32.

Which is a credit card security feature to prevent duplication?

(a) logo

(b) Hologram

(c) signature

(d) CW

Answer:

(b) Hologram

![]()

Question 33.

CVC/CW means ………………….

Answer:

Card Verification Code/ Value

Question 34.

Which is used in contact less transactions.

(a) CVC2

(b) EMV

(c) RFID

(d) PIN

Answer:

(a) CVC2

Question 35.

……………………… is a 3 digit code printed to the left of signature pane to validate the card.

Answer:

CVC/CVV

![]()

Question 36.

How many ways of processing debit card transactions are there?

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(b) 3

Question 37.

Which card is an electronic payment card where the transaction amount is deducted from the card holders Bank account?

(a) Credit card

(b) Debit card

(c) Smart card

(d) Paytm card

Answer:

(b) Debit card

Question 38.

Which is also known as online debit or PIN debit?

(a) EFTPOS

(b) POSEFT

(c) FETPOS

(d) FETSOP

Answer:

(a) EFTPOS

![]()

Question 39.

……………………. is a type of debit card that is preloaded with certain amount.

Answer:

Stored value card

Question 40.

Which is true regarding stored value cards?

(i) It has default monetary value onto it.

(ii) The card may be disposed when the value is used.

(iii) It is used to make offline purchases

(a) (i), (ii), (iii)

(b) (ii), (iii)

(c) (i), (ii)

(d) (iii) alone

Answer:

(a) (i), (ii), (iii)

![]()

Question 41.

How many varieties of stored value card are there?

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(a) 2

Question 42.

Pick the odd one out.

(a) closed loop cards

(b) open loop cards

(c) prepaid-debit cards

(d) visa gift cards

Answer:

(a) closed loop cards

![]()

Question 43.

In which of the following cards in binary coded metaphorically stored on the card in binary coded data form?

(a) open loop cards

(b) prepaid-debit cards

(c) closed loop cards

(d) visa gift cards

Answer:

(c) closed loop cards

Question 44.

Which of the following is not the advantage of smart cards?

(a) Identification

(b) RFID

(c) datastorage

(d) application processing

Answer:

(b) RFID

![]()

Question 45.

Smart cards are classified into ……………………. types.

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(a) 2

Question 46.

The two classifications of smart cards are ……………………… and ………………….. smart cards.

Answer:

contact and contactless

Question 47.

POS stands for ………………………

Answer:

Point of Sale

Question 48.

Contact smart cards have a contact area of approximately ……………………….

(a) 1 cms2

(b) 10 cms2

(c) 1 mm2

(d) 1 hectares

Answer:

(a) 1 cms2

![]()

Question 49.

Find the statements which is not true?

(I) contact smart cards uses RF induction Technology

(II) smarts have Internal power Source

(III) Inductor is used to capture radio-frequency signal

(a) I, II

(b) II, III

(c) I, II

(d) III

Answer:

(c) I, II

Question 50.

Which technology is used in contactless smart cards.

(a) UV Induction

(b) RF Induction

(c) RFID

(d) IRID

Answer:

(b) RF Induction

![]()

Question 51.

EFT means ………………………

Answer:

Electronic Funds Transfers

Question 52.

RTGS means …………………….

Answer:

Real Time Gross Settlement System

Question 53.

ECS ………………….. is used for making bulk payment of amounts.

Answer:

credit

![]()

Question 54.

ECS ………………….. is used for bulk collection of amounts.

Answer:

debit

Question 55.

Identify the wrongly matched pair.

(a) EFPOS – PIN debit

(b) Offline debit – Signature debit

(c) ECS credit – Push transactions

(d) ECS debit – Pull transactions

Answer:

(a) EFPOS – PIN debit

Question 56.

EFT means

(a) National Electronic Fund Transactions

(b) National Electronic Fund Transfer

(c) National Electronic Finance Technology

(d) National Electronic Financial Transactions

Answer:

(b) National Electronic Fund Transfer

![]()

Question 57.

RBI means ……………………..

Answer:

Reserve Bank of India

Question 58.

IDRBT stands for ……………………

Answer:

Institute for Development and Research in Banking Technology

Question 59.

NEFT initiated in the year ……………………..

(a) 2001

(b) 2003

(c) 2005

(d) 2009

Answer:

(c) 2005

![]()

Question 60.

Which one of the following enables bank customer to transfer funds between any two banks?

(a) EFT

(b) NEFT

(c) EMI

(d) ECS

Answer:

(b) NEFT

Question 61.

…………………… payments are generally large-value payments

Answer:

RTGS

Question 62.

…………………… is the electronic transfer of money over an online network

Answer:

EFT

Question 63.

Which one of the following is the currency that flows in the form of data?

(a) RTGS

(b) EFT

(c) ECS

(d) E-cash

Answer:

(d) E-cash

![]()

Question 64.

Cryptocurrency is also called as …………………..

(a) Cryptocoins

(b) e-cahs

(c) virtual currencies

(d) all of these

Answer:

(d) all of these

Question 65.

The state of ownership of a cryptocurrency is related to individual system blocks called ………………………

(a) portfolios

(b) virtual asset

(c) erytography

(d) none of these

Answer:

(a) portfolios

![]()

Question 66.

What are the technologies used in cryptocurrency?

(a) Mining

(b) block chain

(c) Directed Acyclic Graph

(d) All of these

Answer:

(d) All of these

Question 67.

The first form of cryptocurrency is ……………………….

(a) Digicash

(b) D-cash

(c) E-cash

(d) Crypto cash

Answer:

(a) Digicash

Question 68.

“Digicash” was invented by …………………….

Answer:

David Chaum

Question 69.

Digicash was invented in the year ………………………

(a) 1978

(b) 1980

(c) 1985

(d) 1989

Answer:

(d) 1989

![]()

Question 70.

Identify the wrongly matched pair.

(a) Digicash- 1989

(b) Bitcoin- 2009

(c) SHA-254-crytographic Hash function

(d) Altcoin – 2011

Answer:

(c) SHA-254-crytographic Hash function

Question 71.

Which is the most popular and the first decentralized cryptocurrency?

(a) Digicash

(b) Bitcoin

(c) Altcoins

(d) block chain

Answer:

(b) Bitcoin

Question 72.

Bitcoin payment system was developed under the pseudonym ……………………….

Answer:

Satosi Nakamoto

![]()

Question 73.

………………….. was developed to build alternative root DNS servers.

Answer:

Namecoin

Question 74.

Which cryptocurrency has a higher transaction rate?

(a) Altcoin

(b) Litecoin

(c) Bitcoin

(d) Namecoin

Answer:

(b) Litecoin

Question 75.

Making few minor changes in the parameters of cryptocurrency is called ………………………..

(a) altoin

(b) Block

(c) Blockchain

(d) Fork

Answer:

(d) Fork

![]()

Question 76.

As the value of altcoins becomes ………………….. it is considered as dead.

(a) Null

(b) 0

(c) infinity

(d) negative

Answer:

(b) 0

Question 77.

Pick the odd one out.

(a) Bitshares

(b) Mastercoin

(c) Ripple

(d) Nxt

Answer:

(c) Ripple

Question 78.

Pick the odd one out.

(a) Monera

(b) Nxt

(c) Ethereum

(d) Mastercoin

Answer:

(d) Mastercoin

![]()

Question 79.

The Cryptocurrency units are created by the solution of cryptographic tasks called ………………………..

(a) mining

(b) Block chain

(c) Hash

(d) Brick and Mortar

Answer:

(a) mining

Question 80.

Find the statements which are not true.

(i) The miners generate new monetary units

(ii) Miners doesh’t initiate new transactions

(iii) Miners receive new Bitcoins

(a) (i)

(b) (iii)

(c) (ii)

(d) All are true

Answer:

(c) (ii)

Question 81.

ICO means ……………………….

Answer:

Intial coin offer

![]()

Question 82.

Which one of the following are an open distributed book that records transactions of crypto currencies?

(a) mining

(b) e-wallets

(c) ICO

(d) Block chains

Answer:

(d) Block chains

Question 83.

Each block in the block chain contains ………………….. pointer

(a) dash

(b) hash

(c) memory

(d) link

Answer:

(b) hash

![]()

Question 84.

Which one of the following is an electronic wallet services?

(a) paypal

(b) block chain

(c) mining

(d) hash

Answer:

(a) paypal

Question 85.

The term mobile banking is also called ………………………

Answer:

m-banking

Question 86.

……………………. operates only on the Internet with no physical branches.

Answer:

virtual banking

Question 87.

OTP means ……………………….

Answer:

One-Time Password

Question 88.

PJN means ……………………

Answer:

Personal Identification Number

![]()

Question 89.

ACHmeans …………………….

Answer:

Automated Clearing Home

Question 90.

IFSC stands for ……………………

Answer:

Indian Financial System Code

Question 91.

……………………… is an 11 digit alpha-numeric code issued Reserve Bank of India

(a) IIT

(b) IIM

(c) IFSC

(d) IFCS

Answer:

(c) IFSC

Question 92.

UPI means ………………………

Answer:

Unified Payments

![]()

Question 93.

NCPI means …………………..

Answer:

National Payments Corporation of India

Question 94.

Unified Payments Interface is a real time payment system developed by NCPI to facilitate inter-bank transactions.

Answer:

Unified Payments Interface

Question 95.

IMPS stands for ………………………

Answer:

Immediate Payment Service

Question 96.

UPI applications …………………………. types of address.

(a) 2

(b) 3

(c) 4

(d) 5

Answer:

(a) 2

![]()

Question 97.

UPI applications are classified into two types of addresses like …………………….. and ……………………

Answer:

global and local

Question 98.

Which address in UPI is a virtual payment address?

(a) Global

(b) local

(c) private

(d) public

Answer:

(b) local

Question 99.

………………… also called as UPI-ID.

Answer:

Virtual Payment Address(VPA)

Question 100.

MPIN means ……………………..

Answer:

Mobile Banking Personal Identification Number

![]()

Question 101.

USSD means …………………..

Answer:

Unstructured Supplementary Service Data

Question 102.

COD means …………………..

Answer:

Cash on Delivery

Question 103.

BHIM stands for …………………….

Answer:

Bharat Interface for Money

Question 104.

NPCI means …………………….

Answer:

National Payments Corporation of India

Question 105.

BHIM is an exclusive mobile app for UPI developed by ……………………..

(a) 2014

(b) 2015

(c) 2016

(d) 2017

Answer:

(c) 2016

![]()

Question 106.

……………………. is a type of fraud where same cryptocurrency is spent in more than one transactions.

Answer:

Double Spend

Question 107.

RThs are …………………. and ……………………

Answer:

Unconditional, Irrevocable

II. Short Answer

Question 1.

Write note on payment cards?

Answer:

Payment cards are plastic cards that enable cashless payments. They are simple embossed plastic card that authenticates the card holder on behalf of card issuing company, which allows the user to make use of various financial services.

![]()

Question 2.

Give some examples for macro online payment systems?

Answer:

Some of the popular macro on-line payment systems are mentioned below:

- Card based payment systems

- Electronic account transfer

- Electronic cash payment systems

- Mobile payment systems and internet payment systems

Question 3.

Write note on E-cash?

Answer:

Electronic cash is (E-Cash) is a currency that flows in the form of data. It converts the cash value into a series of encrypted sequence numbers, and uses these serial numbers to represent the market value of various currencies in reality.

![]()

Question 4.

Mention the advantages of UPI?

Answer:

- Immediate money transfers through mobile device round the clock 24 × 7.

- Can use single mobile application for accessing multiple bank accounts,

- Single Click Authentication for transferring of fund.

- It is not required to enter the details such as Card no, Account number, IFSC etc. for every transaction.

- Electronic payments will become much easier without requiring a digital wallet or credit or debit card.

Question 5.

Define COD?

Answer:

Cash on delivery (COD) also called as collection on delivery, describes a mode of payment in which the payment is made only on receipt of goods rather in advance.

![]()

Question 6.

Define BHIM?

Answer:

Bharat Interface for Money (BHIM) is an exclusive mobile app for UPI developed by National Payments Corporation of India (NPCI) and launched on 30 December 2016. It is intended to facilitate e-payments directly through banks and drive towards cashless transactions.

III. Explain in Brief Answer

Question 1.

How will you do the Micro electronic payment transactions?

Answer:

In general, the parties involved in the micro on-line payments are Customer, Service Provider and Payment processor. The Micro electronic payment transactions can be explained in the following way.

Step 1:

Customer proves his authentication and the payment processor issues micro payments.

Step 2:

Customer pays the micro payments to the online service provider and gets the requested goods or services form them.

Step 3:

Service provider deposits micro payments received from the customer to the payment processor and gets the money.

![]()

Question 2.

Mention the three types of card based payment systems?

Answer:

Based on the transaction settlement method there are three widely used card based payment systems. They are:

- Credit card based payment systems (pay later)

- Debit card based payment systems (pay now)

- Stored value card based payment systems (pay before)

Question 3.

Mention the advantages of credit card?

Answer:

Advantages of credit card:

- Most credit cards are accepted worldwide.

- It is not necessary to pay physical money at the time of purchase. The customer gets an extra period to pay the purchase.

- Depending on the card, there is no need to pay annuity.

- Allows purchases over the Internet in installments.

- Some issuers allows “round up” the purchase price and pay the difference in cash to make the transactions easy.

![]()

Question 4.

Write note on ‘The Diner Club Card’?

Answer:

In February 1950, Frank McNamara and Ralph Schneider created The Diners Club card which was made of paper-cardboard. Initially The card was accepted in only 27 restaurants From 1955, the card was made of plastic. The Diners Club still exists today under the name Diners Club International.

Question 5.

Write note on Anatomy of a Credit Card?

Answer:

All Payment cards (including debit card) are usually plastic cards of size 85.60 mm width x 53.98 mm height, rounded comers with a radius of 2.88 mm to 3.48 mm and thickness of 0.76 mm.

Question 6.

Write note on Credit Card number?

Answer:

Credit card number:

The modem credit card number has 16-digit unique identification number.

![]()

Question 7.

Mention the three ways of processing debit card transactions?

Answer:

There are three ways of processing debit card transactions:

- EFTPOS (also known as online debit or PIN debit)

- Offline debit (also known as signature debit)

- Electronic Purse Card System

Question 8.

Mention the major advantage of stored value card?

Answer:

The major advantage of stored value card is that customers don’t need to have a bank account to get prepaid cards.

![]()

Question 9.

Write note on Smart Card?

Answer:

Smart cards along with the regular features of any card based payment system holds a EMV chip. This chip is similar to well-known sim card in appearance.

Question 10.

Mention the advantages of Smart Cards?

Answer:

The advantage of Smart cards is that it can provide identification, authentication, data storage and application processing.

Question 11.

Write note on ECS debit?

Answer:

ECS debit:

ECS debit is an inverse of ECS credit. It is used for bulk collection of amounts. In this mode, multiple accounts are debited and then a single account is credited. This type of transactions are Pull transactions. Example: The insurance premium of bulk number of customers.

![]()

Question 12.

Write note on NEFT?

Answer:

(NEFT) is an electronic funds transfer system initiated by the Reserve Bank of India (RBI) in – November 2005. NEFT enables a bank customer to transfer funds between any two NEFT- enabled bank accounts on a one-to-one basis. It is done via electronic messages.

Question 13.

Give the two types of Real-time gross settlement transactions?

Answer:

Real-time gross settlement transactions are:

Unconditional – the beneficiary will receive funds regardless of whether he fulfills his obligations to the buyer or whether he would deliver the goods or perform a service of a quality consistent with the order.

Irrevocable – a correctly processed transaction cannot be reversed and its money cannot get refunded (the so-called settlement finality).

![]()

Question 14.

How are the Mobile Banking operations implemented?

Answer:

Mobile Banking operations can be implemented in the following ways:

- Contacting the call center.

- Automatic IVR telephone service.

- Using a mobile phone via SMS.

- WAP technology

- Using smartphone applications.

Question 15.

Mention advantages of Internet Banking?

Answer:

1. The advantages of Internet banking are that the payments are made at the convenience of the account holder and are secured by user name and password, i.e. with Internet access it can be used from anywhere in the world and at any time.

2. Any standard browser (e.g. Google Chrome) is adequate. Internet banking does not need installing any additional software.

![]()

Question 16.

Explain the two types of addresses in UPI applications?

Answer:

UPI applications use two types of address – global and local.

- Global address includes bank account numbers and IFSC.

- Local address is a virtual payment address.

IV. Explain in detail

Question 1.

Explain Debit Card?

Answer:

Debit Card:

Debit Card is an electronic payment card where the transaction amount is deducted directly from the card holder’s bank account upon authorization.

Generally, debit cards function as ATM cards and act as a substitute for cash The way of using debit cards and credit cards is generally the same but unlike credit cards, payments using a debit card are immediately transferred from the cardholder’s designated bank account, instead of them paying the money back at a later with added interest. In modem era the use of debit cards has become so widespread’.

The debit card and credit card are identical in their physical properties. It is difficult to differentiate two by their appearance unless they have the term credit or debit imprinted. Currently there are three ways of processing debit card transactions:

- EFTPOS (also known as online debit or PIN debit)

- Offline debit (also known as signature debit)

- Electronic Purse Card System 2. Explain Smart

![]()

Question 2.

Explain Smart Card?

Answer:

Smart card:

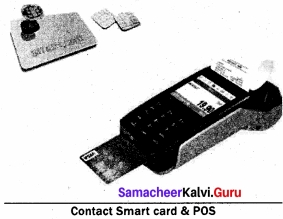

The modem version of card based payment is smart cards. Smart cards along with the regular features of any card based payment system holds a EMV chip.

This chip is similar to well-known sim card in appearance but differ in its functionalities. The advantage of Smart cards is that it can provide identification, authentication, data storage and application processing. Smart cards can be classified into Contact smart cards and Contactless smart, Contact Smart card & POS cards.

(i) Contact smart cards:

Contact smart cards have a contact area of approximately 1 square centimeter, comprising several gold – plated contact pads. These pads provide electrical connectivity only when inserted into a reader, which is also used as a communications medium between the smart card and a host. e.g. a point of sale terminal(POS).

(ii) Contactless smart cards:

Contactless smart card is empowered by RF induction technology. Unlike contact smart cards, these cards require only near proximity to an antenna to communicate. Smart cards, whether they are contact or contactless cards do not have an internal power source. Instead, they use an inductor to capture some of the interrupting radio-frequency signal, rectify it and power the card’s processes.