Students can Download Accountancy Chapter 1 Accounts from Incomplete Records Questions and Answers, Notes Pdf, Samacheer Kalvi 12th Accountancy Book Solutions Guide Pdf helps you to revise the complete Tamilnadu State Board New Syllabus and score more marks in your examinations.

Tamilnadu Samacheer Kalvi 12th Accountancy Solutions Chapter 1 Accounts from Incomplete Records

Samacheer Kalvi 12th Accountancy Accounts from Incomplete Records Text Book Back Questions and Answers

I. Choose the Correct Answer

Question 1.

Incomplete records are generally maintained by …………….

(a) A company

(b) Government

(c) Small sized sole trader business

(d) Multinational enterprises

Answer:

(c) Small sized sole trader business

Question 2.

Statement of affairs is a …………….

(a) Statement of income and expenditure

(b) Statement of assets and liabilities

(c) Summary of cash transactions

(d) Summary of credit transactions

Answer:

(b) Statement of assets and liabilities

![]()

Question 3.

Opening statement of affairs is usually prepared to find out the …………….

(a) Capital in the beginning of the year

(b) Capital at the end of the year

(c) Profit made during the year

(d) Loss occurred during the year

Answer:

(a) Capital in the beginning of the year

Question 4.

The excess of assets over liabilities is …………….

(a) Loss

(b) Cash

(c) Capital

(d) Profit

Answer:

(c) Capital

Question 5.

Which of the following items relating to bills payable is transferred to total creditors account?

(a) Opening balance of bills payable

(b) Closing balance of bills payable

(c) Bills payable accepted during the year

(d) Cash paid for bills payable

Answer:

(c) Bills payable accepted during the year

Question 6.

The amount of credit sales can be computed from …………….

(a) Total debtors account

(b) Total creditors account

(c) Bills receivable account

(d) Bills payable account

Answer:

(a) Total debtors account

Question 7.

Which one of the following statements is not true in relation to incomplete records?

(a) It is an unscientific method of recording transactions

(b) Records are maintained only for cash and personal accounts

(c) It is suitable for all types of organisations

(d) Tax authorities do not accept

Answer:

(c) It is suitable for all types of organisations

Question 8.

What is the amount of capital of the proprietor, if his assets are ₹ 85,000 and liabilities are ₹ 21,000?

(a) ₹ 85,000

(b) ₹ 1,06,000

(c) ₹ 21,000

(d) ₹ 64,000

Answer:

(d) ₹ 64,000

![]()

Question 9.

When capital in the beginning is ₹ 10,000, drawings during the year is ₹ 6,000, profit made during the year is ₹ 2,000 and the additional capital introduced is ₹ 3,000, find out the amount of capital at the end …………….

(a) ₹ 9,000

(b) ₹ 11,000

(c) ₹ 21,000

(d) ₹ 3,000

Answer:

(a) ₹ 9,000

Question 10.

Opening balance of debtors: ₹ 30,000, cash received: ₹ 1,00,000, credit sales: ₹ 90,000; closing balance of debtors is …………….

(a) ₹ 30,000

(b) ₹ 1,30,000

(c) ₹ 40,000

(d) ₹ 20,000

Answer:

(d) ₹ 20,000

II. Very Short Answer Questions

Question 1.

What is meant by incomplete records?

Answer:

When accounting records are not strictly maintained according to double entry systems, these records are called incomplete accounting records.

Question 2.

State the accounts generally maintained by the small-sized sole trader when a double-entry accounting system is not followed.

Answer:

Generally, cash account and the personal accounts of customers and creditors are maintained by small-sized sole trader. When the double-entry accounting system is not followed.

![]()

Question 3.

What is a statement of affairs?

Answer:

A statement of affairs is a statement showing the balances of assets and liabilities on a particular date. It is prepared when accounts are maintained under a single entry system to find out the capital of the business.

III. Short Answer Questions

Question 1.

What are the features of incomplete records?

Answer:

Following are the features of incomplete records:

- Nature: It is an unscientific and unsystematic way of recording transactions. Accounting principles and accounting standards are not followed properly.

- Type of accounts maintained: In general, only cash and personal accounts are maintained fully. Real accounts and nominal accounts are not maintained properly. Some transactions are completely omitted.

- Lack of uniformity: There is no uniformity in recording the transactions among different organizations. Different organizations record their transactions according to their needs and conveniences.

![]()

Question 2.

What are the limitations of incomplete records?

Answer:

Limitations of Incomplete records:

1. Lack of proper maintenance of records – It is an unscientific and unsystematic way of maintaining records. Real and nominal accounts are not maintained properly.

2. Difficulty in preparing trial balance – As accounts are not maintained for all items, the accounting records are incomplete. Hence, it is difficult to prepare trail balance to check the arithmetical accuracy of accounts.

3. Difficulty in ascertaining true profitability of the business – Profit is found out based on available information and estimates. Hence, it is difficult to prepare ascertain true profit as the trading and profit and loss account cannot be prepared with accuracy.

4. Difficulty in ascertaining financial position – In general, only the estimated values of assets and liabilities are available from incomplete records. Hence, it is difficult to ascertain true and fair view of state of affairs or financial position as on a particular date

5. Errors and frauds cannot be detected easily – As only partial records are available, it may not be possible to have internal checks in maintaining accounts to detect errors and frauds.

6. Unacceptable to government and other activities – As accounts maintained are incomplete, these may not comply with the legal requirements. Hence, government, tax authorities, and other legal authorities do not accept accounts prepared from incomplete records.

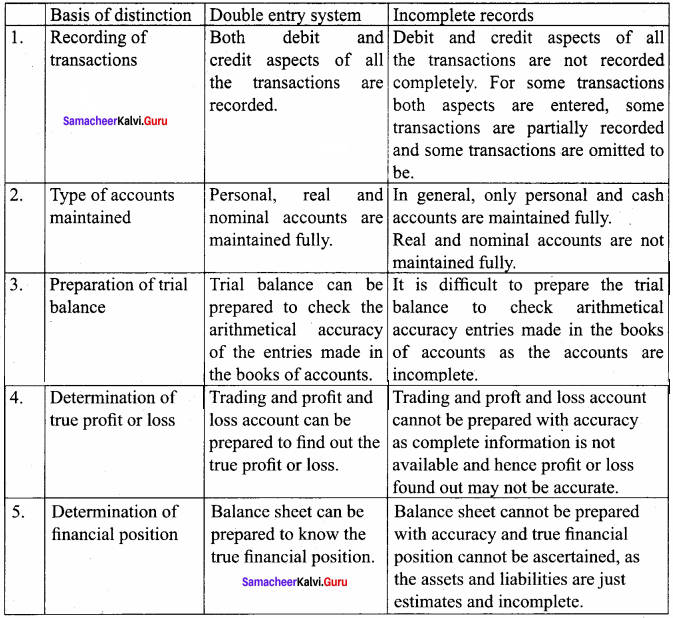

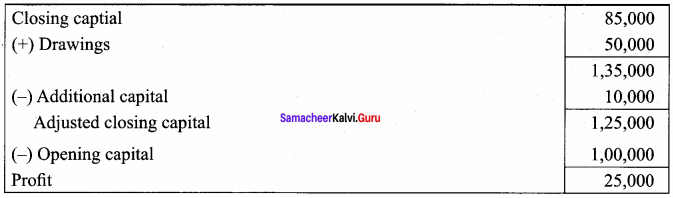

Question 3.

State the differences between double-entry system and incomplete records.

Answer:

Question 4.

State the procedure for calculating profit or loss through the statement of affairs.

Answer:

Under this method, by comparing the capital (net worth) at the beginning and at the end of a specified period profit or loss is found out. Any increase in capital (net worth) is taken as profit while a decrease in capital is regarded as a loss.

Capital at the beginning and at the end can be found out by preparing the statement of affairs at the beginning and at the end of an accounting year respectively.

The difference between the closing capital and the opening capital is taken as profit or loss of the business. Due adjustments are to be made for any withdrawal of capital from the business and for the additional capital introduced in the business.

Closing Capital + Drawings – Additional Capital – Opening Capital = Profit / Loss

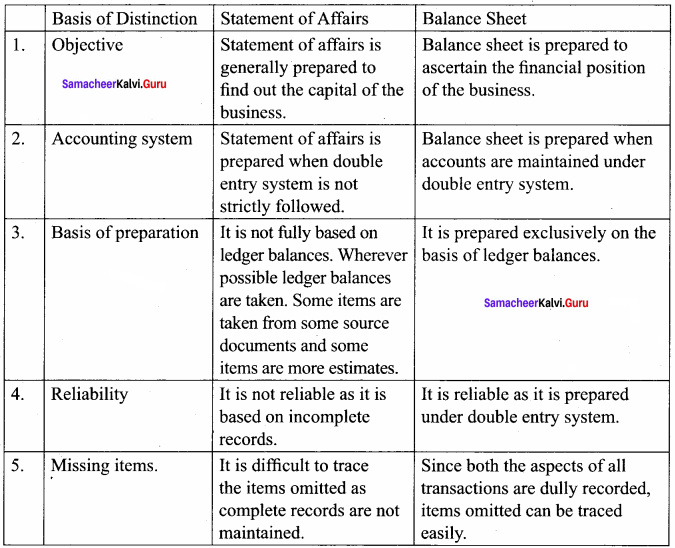

Question 5.

Differentiate between the statement of affairs and the balance sheet.

Answer:

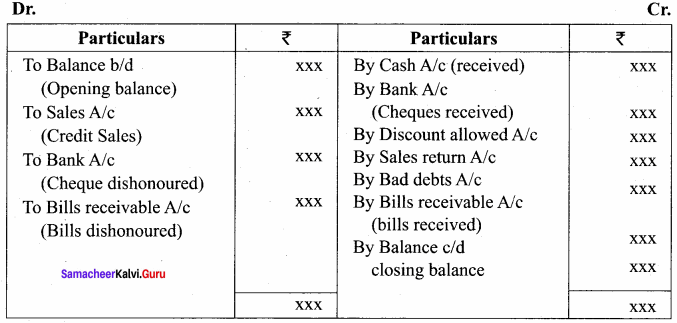

Question 6.

How is the amount of credit sale ascertained from incomplete records?

Answer:

Ascertainment of Credit Sales:-

IV. Exercises:

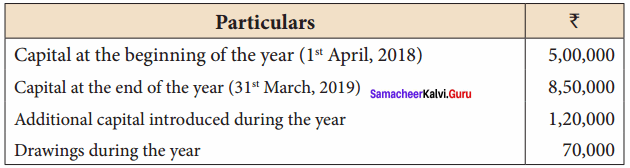

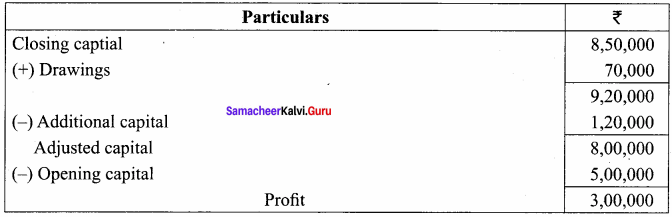

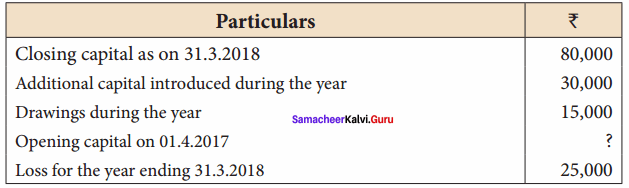

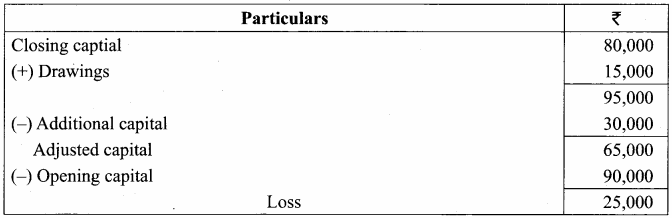

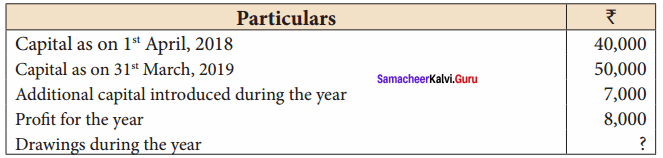

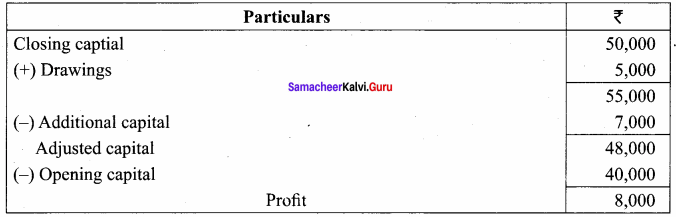

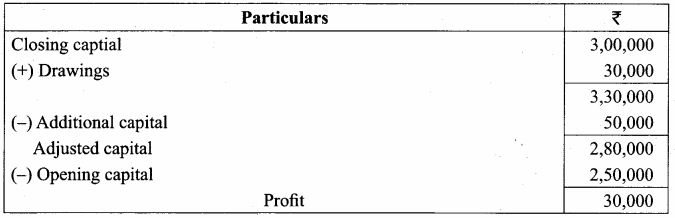

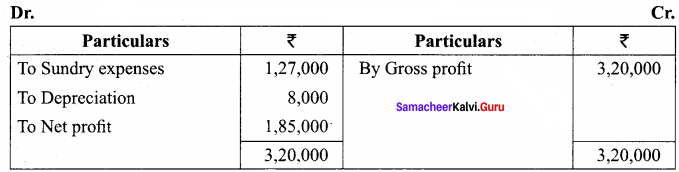

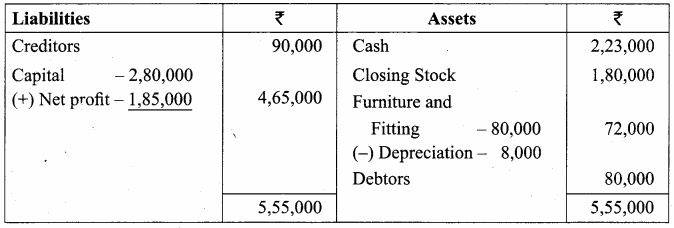

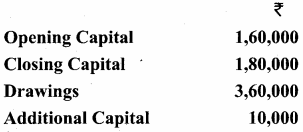

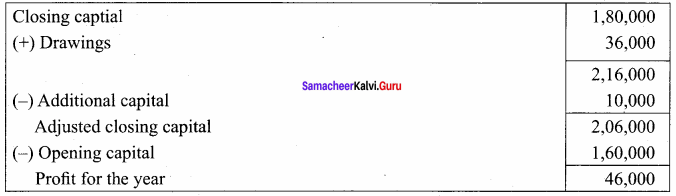

Question 1.

From the following particulars ascertain profit or loss:

Answer:

Statement of profit or Loss

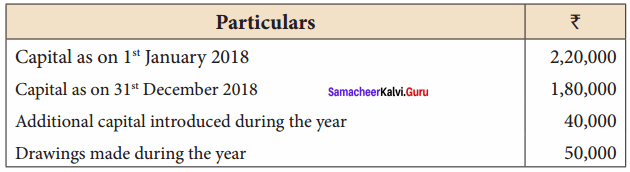

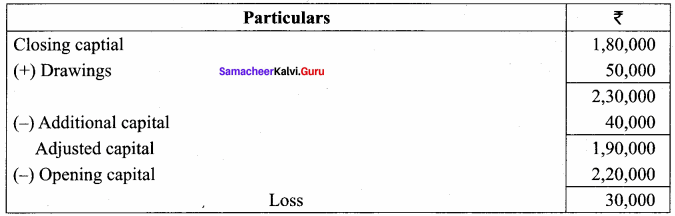

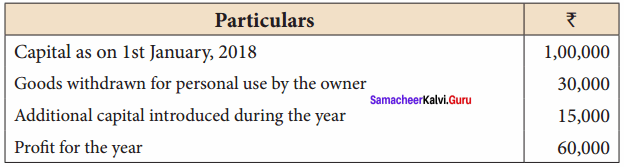

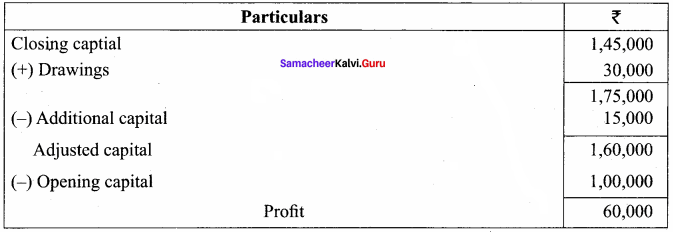

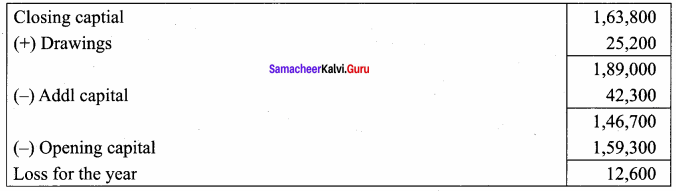

Question 2.

From the following particulars ascertain profit or loss:

Answer:

Statement of Profit or Loss

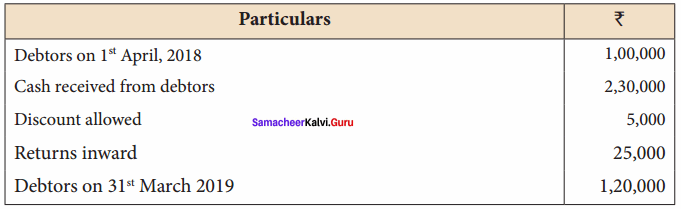

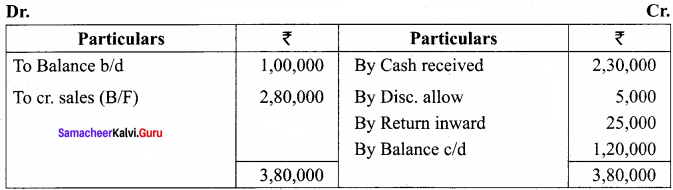

Question 3.

From the following details, calculate the missing figure:

Answer:

Statement of Profit or Loss

Question 4.

From the following details, calculate the capital as of 31st December 2018.

Answer:

Statement of Profit or Loss

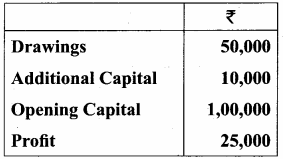

Question 5.

From the following details, calculate the missing figure:

Answer:

Statement of Profit or Loss

Question 6.

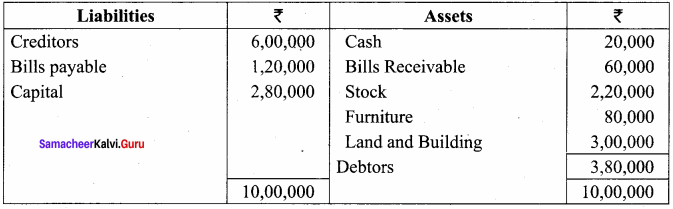

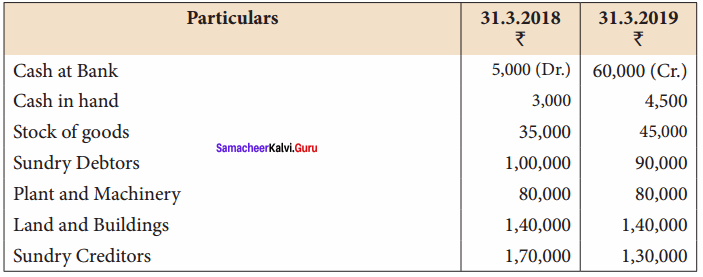

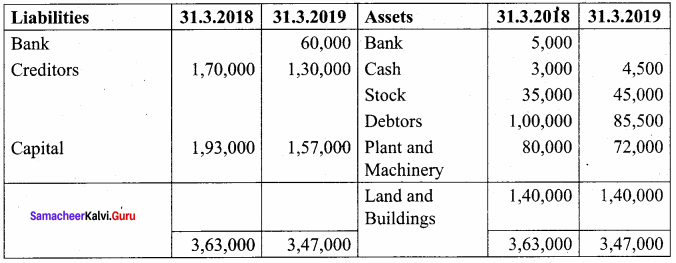

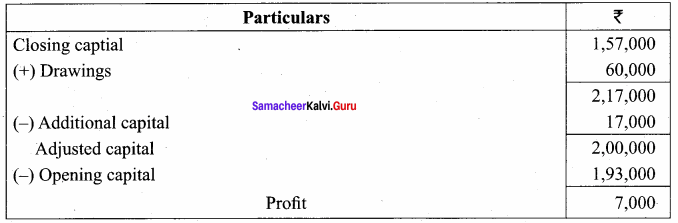

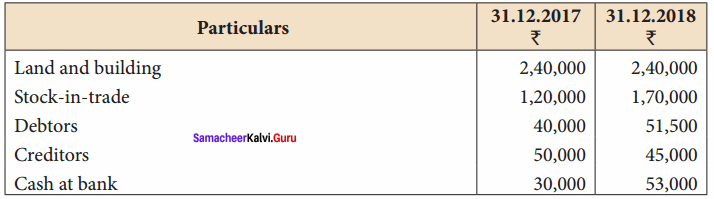

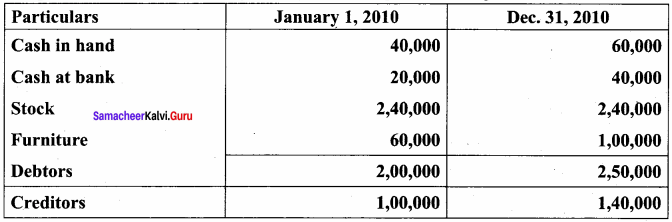

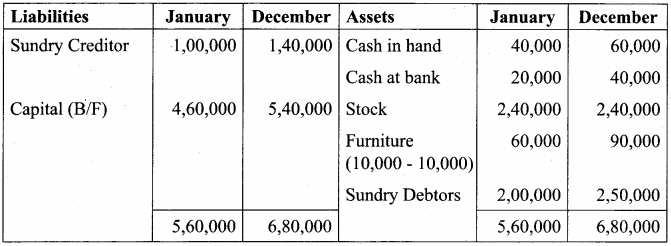

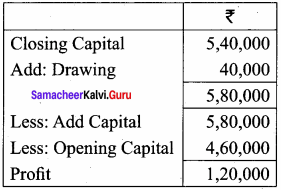

Following are the balances in the books of Thomas as of 31st March 2019.

Prepare a statement of affairs as of 31st March 2019 and calculate capital as of that date.

Answer:

Statement of Profit or Loss

Question 7.

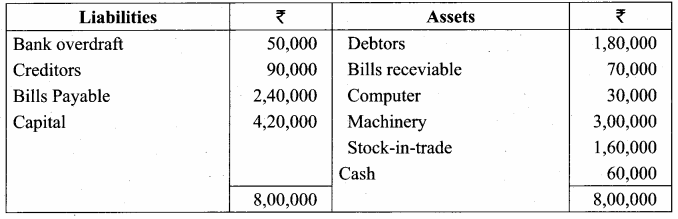

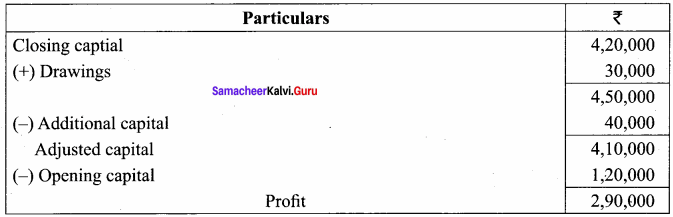

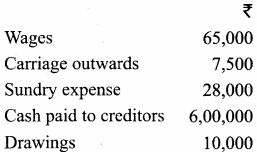

On 1st April 2018 Subha started her business with a capital of ₹ 1,20,000. She did not maintain a proper book of accounts. Following particulars are available from her books as of 31.3.2019.

During the year she withdrew ₹ 30,000 for her personal use. Did she introduce further capital of Rs. 40,000 during the year. Calculate her profit or loss.

Answer:

Statement of Affairs

Statement of Profit or Loss

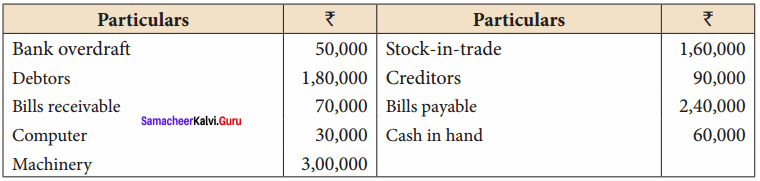

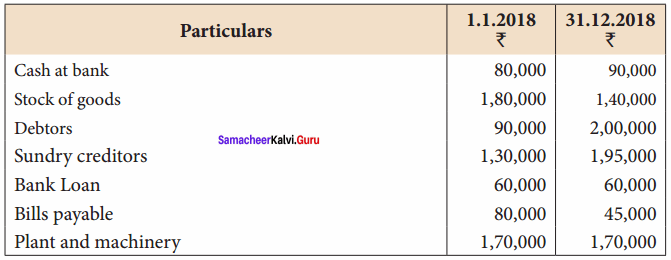

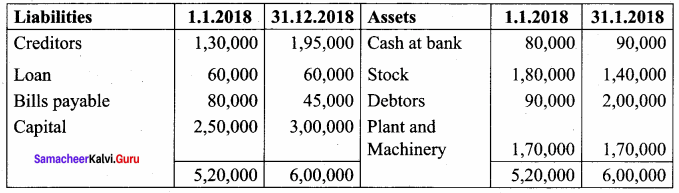

Question 8.

Raju does not keep proper books of accounts. The following details are taken from his records.

During the year he introduced further capital of ₹ 50,000 and withdrew ₹ 2,500 per month from the business for his personal use. Prepare a statement of profit or loss with the above information.

Answer:

Statement of Affairs

Statement of Profit or Loss

Question 9.

Ananth does not keep his books under the double-entry system. Find the profit or loss made by him for the year ending 31st March 2019.

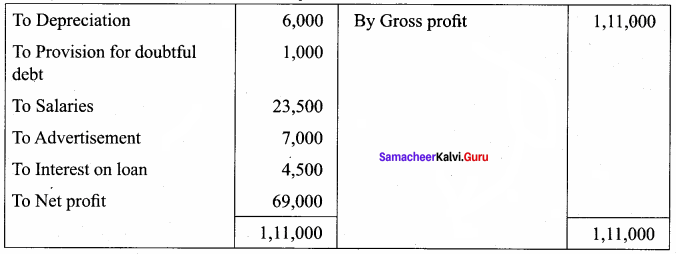

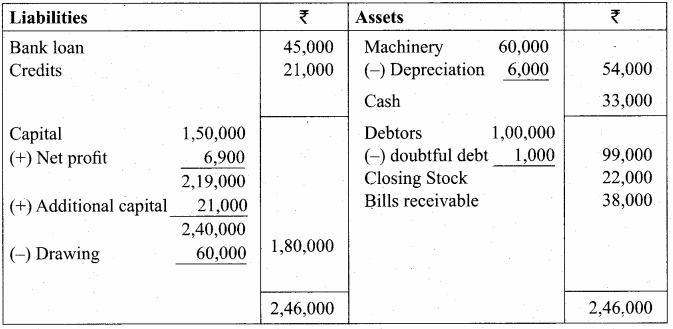

Ananth had withdrawn ₹ 60,000 for his personal use. He had introduced ₹ 17,000 as capita for the expansion of his business. Create a provision of 5% on debtors. Plant and machinery are to be depreciated at 10%.

Answer:

Statement of Affairs

Statement of Profit or Loss

Question 10.

Find out credit sales from the following information:

Answer:

Total / Sundry debtors Account

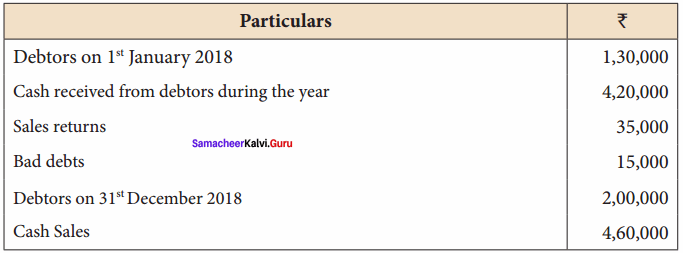

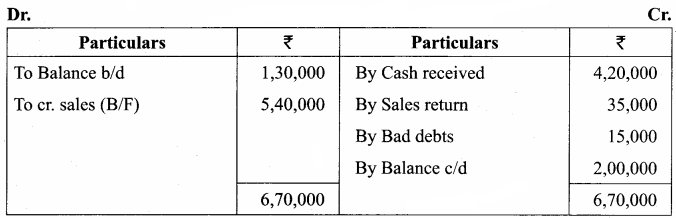

Question 11.

From the following details find out total sales made during the year.

Total / Sundry debtors Account

Total Sales = Cash Sales + Credit Sales

= 4, 60, 000 + 5, 40, 000

= 10, 00, 000

Question 12.

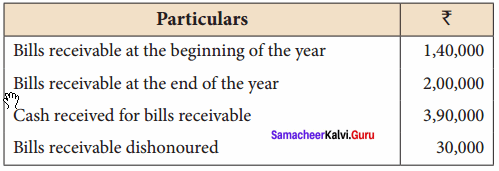

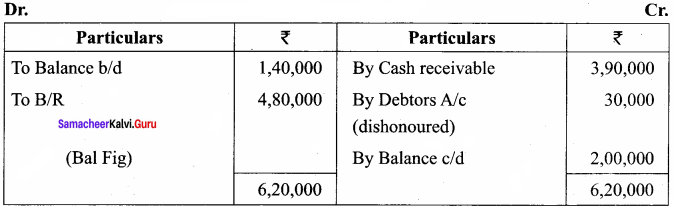

From the following particulars, prepare bills receivable account and compute the bills received from the debtors.

Answer:

Total/Bills Receivable Account

Question 13.

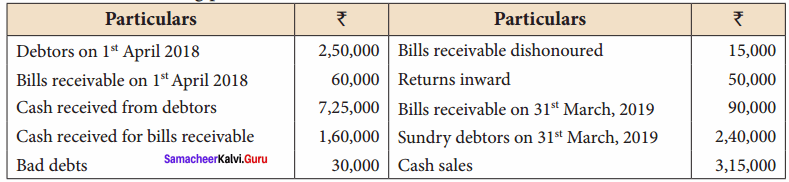

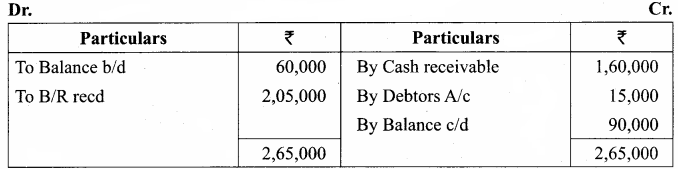

From the following particulars, calculate total sales.

Answer:

Bills Receivable Account

Debtors A/c

Total Sales = Cash Sales + Credit Sales

= 9, 85, 000 + 3, 15, 000

= ₹ 10, 00, 000

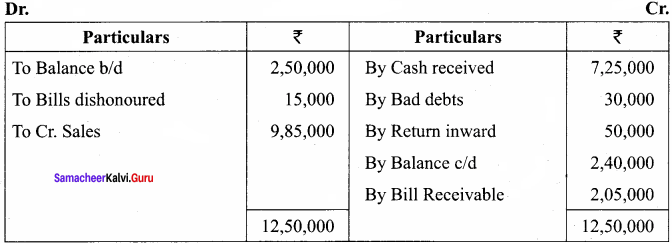

Question 14.

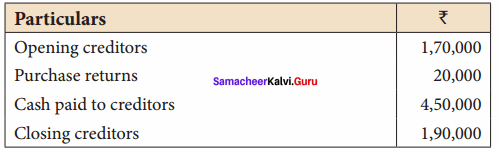

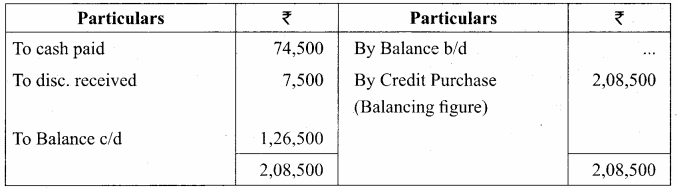

From the following details, calculate credit purchases.

Answer:

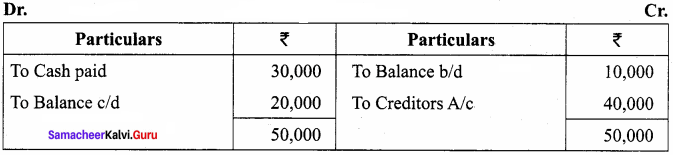

Total/ Sundry Creditors Account

Question 15.

From the following particulars calculate total purchases.

Answer:

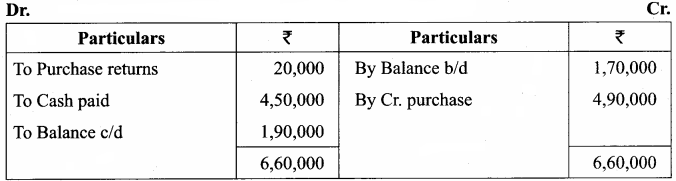

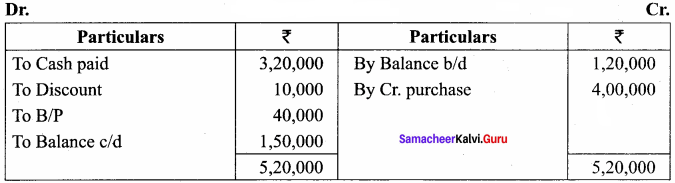

Bills Payable Account

Total Creditors Account

Total purchases = Cash purchases + Credit purchases

Total purchases = 1, 55, 000 + 2, 25, 000

= Rs. 3, 80, 000

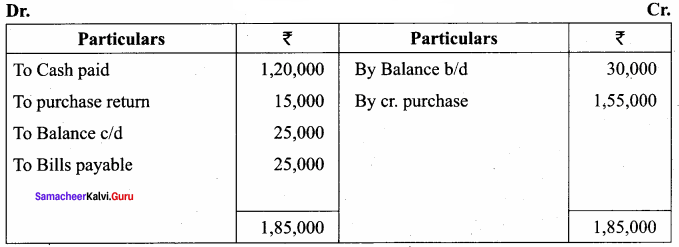

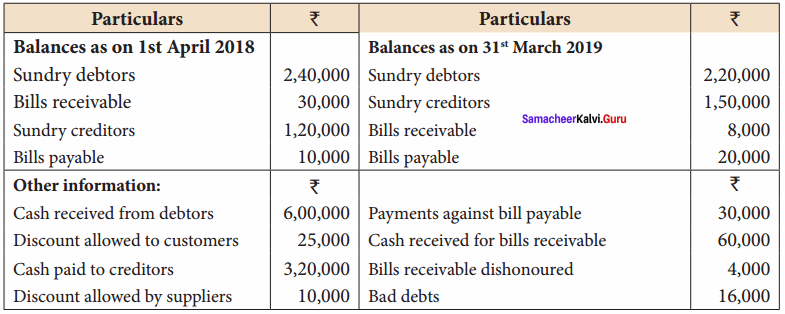

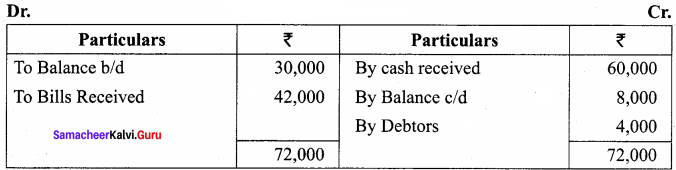

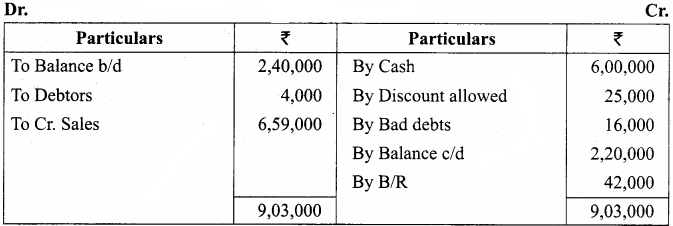

Question 16.

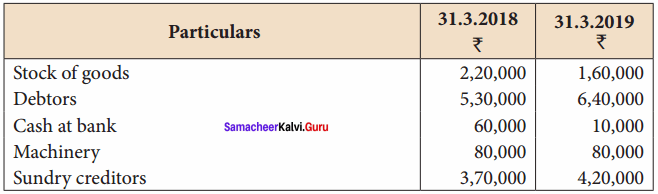

From the following details, you are required to calculate credit sales and credit purchases by preparing total debtors account, total creditors account, bills receivable account, and bills payable account.

Answer:

Bills Receivable A/c

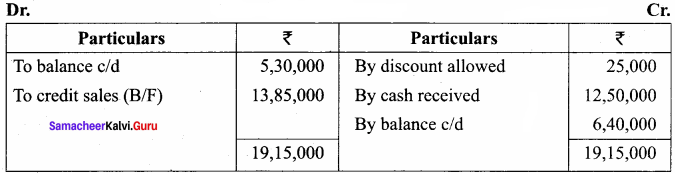

Total debtors A/c

Bills Payable A/c

Total Creditors A/c

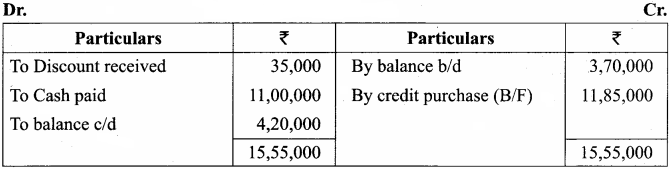

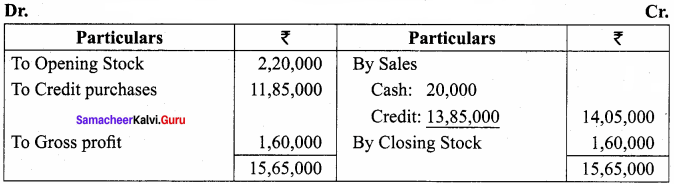

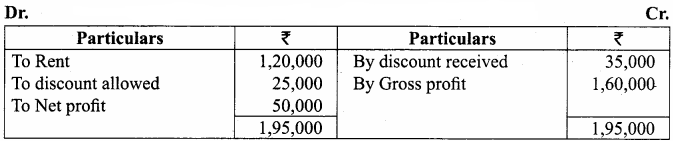

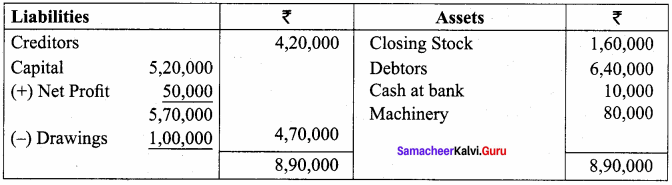

Question 17.

From the following details of Abdul who maintains incomplete records, prepare Trading and Profit and Loss account for the year ended 31st March 2018 and a Balance Sheet as on the date.

Other details:

Answer:

Total Debtors Account

Total Creditors Account

Trading Account for year ended 31st March 2019

Profit/Loss Account for the year ended 31st March 2019

Balance Sheet as on 31st March 2019

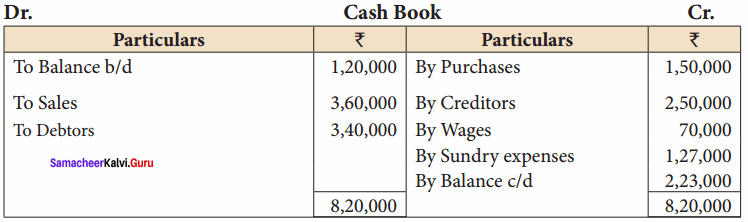

Question 18.

Bharathi does not maintain her books of accounts under the double-entry system. From the following details prepare a trading and profit and loss accounts for the year ending 31st March 2019 and a balance sheet as of that date.

Cash Book

Other information:

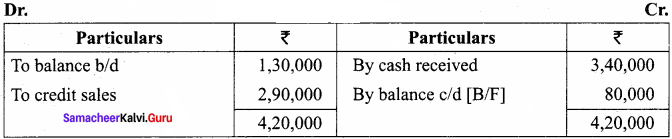

Answer:

Total Debtors Account

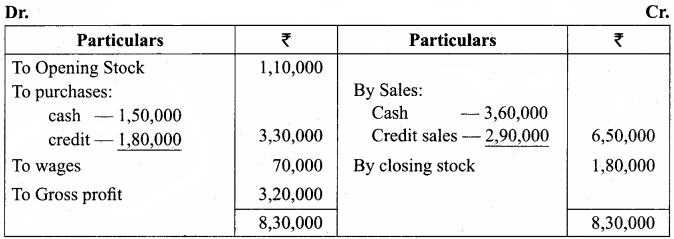

Trading Account for that year ended 31st March 2019

Profit/Loss Account for the year ended 31st March 2019

Balance Sheet as of 31st March 2019

Question 19.

Arjun carries on grocery business and does not keep his books on a double entry basis. The following particulars have been extracted from his books:

Other information for the year ending 31 – 3 – 2019 showed the following:

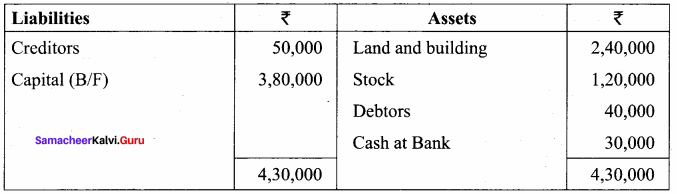

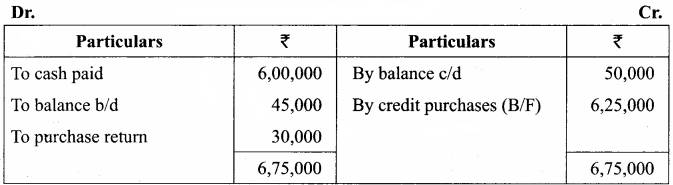

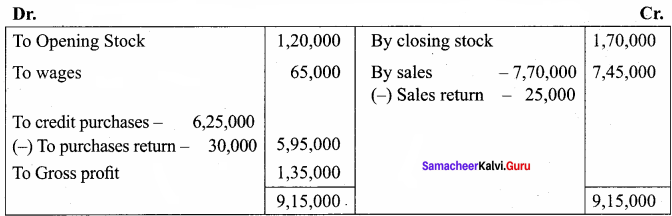

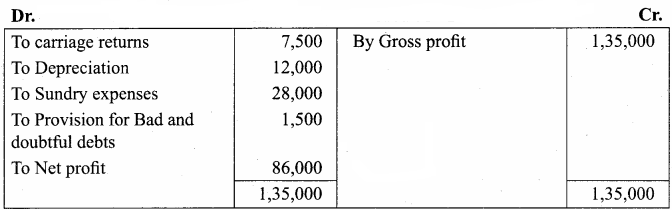

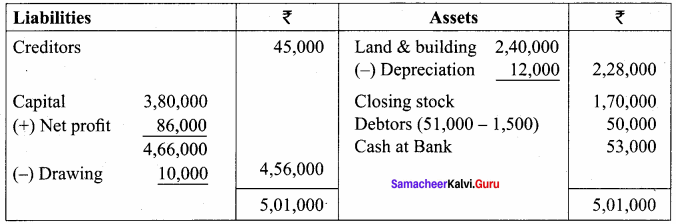

Total sales during the year were ₹ 7, 70,000. Purchases returns during the year were ₹ 30, 000 and sales returns were ₹ 25, 000. Depreciate plant and machinery by 5%. Provide ₹ 1, 500 for doubtful debts. Prepare trading and profit and loss account for the year ending 31st March 2019 and a balance sheet as on the date.

Answer:

Statement of Affairs

Total Credit Account

Trading Account for the year ended 31st December 2019

Profit/Loss Account for the year ended 31st December 2019

Balance Sheet as of 31st December 2019

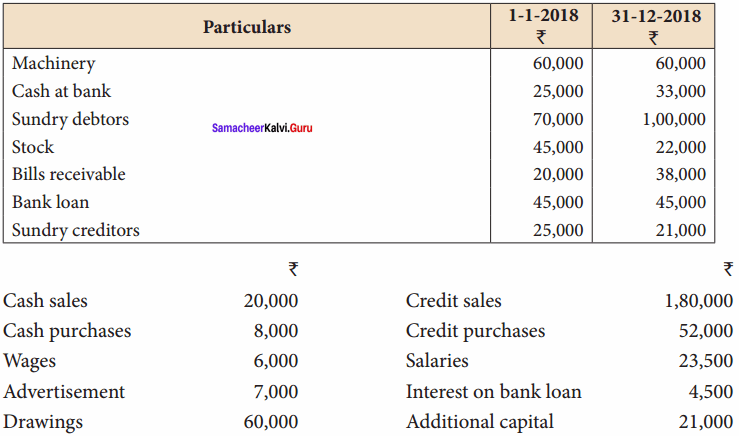

Question 20.

Selvam does not keep his books under the double-entry system. From the following information prepare trading and profit and loss account A/c and balance sheet as of 31 – 12 – 2018.

Adjustments:

Write off the depreciation of 5% on furniture. Create a reserve of 1% on debtors for doubtful debts.

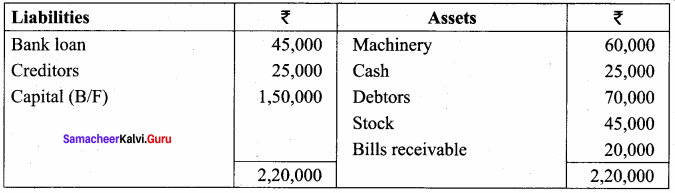

Answer:

Statement of affairs as of 1st January 2018

Answer:

Statement of Affairs as of st January 2018

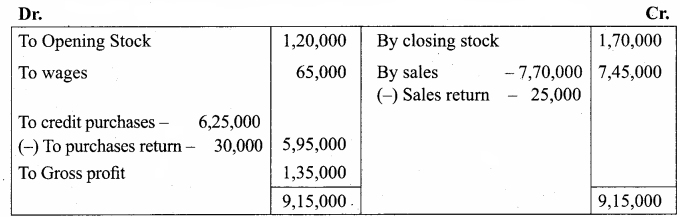

Trading Account for year ended 31st December 2018

Profit/Loss Account for the year ended 31st December 2018

Balance Sheet as on 31st December 2018

Samacheer Kalvi 12th Accountancy Solutions Accounts from Incomplete Records Additional Questions and Answers

I. Choose the correct answer

Question 1.

The single entry system is …………….

(a) a scientific method

(b) an incomplete double entry system

(c) None of these

Answer:

(b) an incomplete double entry system

Question 2.

The single entry system will not be accepted by …………….

(a) Proprietor

(b) Partners

(c) Tax authorities

Answer:

(c) Tax authorities

Question 3.

Single entry system capital is calculated.

(a) Capital = Assets – Liabilities

(b) Assets = Capital – Liabilities

(c) Capital = Assets + Liabilities

(d) Assets = Liabilities – Capital

Answer:

(a) Capital = Assets – Liabilities

![]()

Question 4.

Credit Purchase is obtained from …………….

(a) Total Debtors Accounts

(b) Total Creditors Account

(c) Statement of Affairs

Answer:

(b) Total Creditors Account

Question 5.

Statement of Affairs is like a …………….

(a) Trading Account

(b) Profit and Loss Account

(c) Balance Sheet

Answer:

(c) Balance Sheet

II. Fill in the blanks

Question 6.

Statement of affairs method is also called ……………. method.

Answer:

Networth Method.

Question 7.

A statement of affairs resembles a …………….

Answer:

Balance Sheet.

Question 8.

Single entry system maintains ……………. and ……………. accounts.

Answer:

Cash, Personal.

![]()

Question 9.

A firm has assets worth ₹ 10,00,000 and Capital ₹ 2,25,000 then its liabilities is …………….

Answer:

₹ 7,75,000.

Question 10.

The difference between capital while beginning and capital at the end indicate……………. of the business.

Answer:

Profit/Loss.

Question 11.

The excess of assets over liabilities is …………….

Answer:

Capital.

III. Match the following

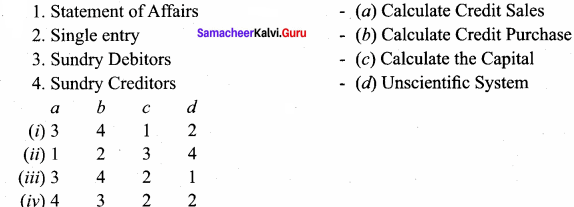

Question 12.

Answer:

(i) 3

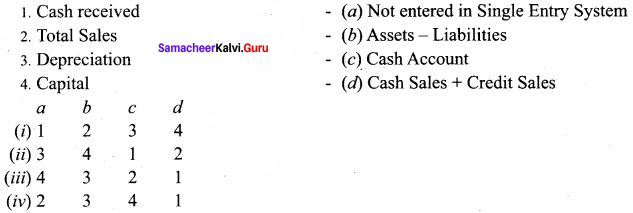

Question 13.

Answer:

(ii) 3

IV. Assertion & Reason

Question 14.

(A) Assertion: Bill receivable endorsed are debited to Creditors Account

(B) Reason: Bills receivable is received from Debtors is credited to Debtors A/c

(a) Both (A) and (B) are correct

(b) (A) is correct and (B) is incorrect

(c) Both are correct

(d) (A) is incorrect but (B) is correct

Answer:

(a) Both (A) and (B) is correct

V. True or False

Question 15.

Limited Companies are free to choose either a single entry (or) Double entry system.

Answer:

False.

Question 16.

Under network, method profit is ascertained by calculating the increase in the network after adjusting for drawing and addition to capital.

Answer:

True.

![]()

Question 17.

Net Profit is calculated to capital at the end + Drawing + Capital introduced – Capital in the beginning.

Answer:

False.

Question 18.

In this system personal accounts and cash accounts transaction is recorded.

Answer:

True.

VI. Very Short Answer Question

Question 1.

Define of Single Entry System.

Answer:

According to Kohler, “Single Entry System is a system of Book-keeping in which as a rule, only records of cash and personal accounts are maintained. It is always an incomplete double entry system varying with circumstances.

VII. Exercise

Question 1.

Calculate the profit for the following information.

Answer:

Question 2.

Calculate opening capital

Answer:

Question 3.

Calculate the missing figure.

Answer:

Question 4.

Joseph maintains books in a single entry. The following details are given from his books.

He has taken ₹ 40,000 from the business for his personal exp depreciate furniture by 10%. Prepare a statement showing profit or loss for the year 2001.

Answer:

Statement of Affairs on 1.1.2010 to 31.12.2010

Statement Profit

Question 5.

From the following details find out the credit purchases and total purchase.

Answer:

Bills Payable Account

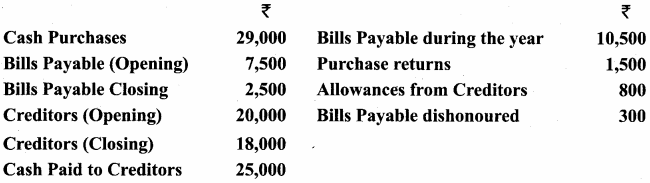

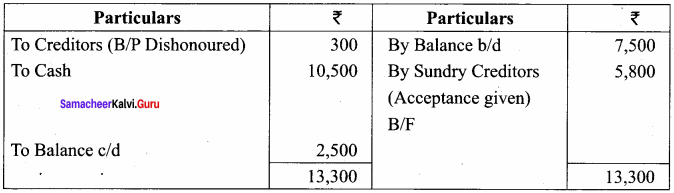

Total Creditors Account

Credit Purchase ₹ 30,800

Total Purchases = Cr Purchases + Cash Purchases

= 30, 800 + 29, 000

= ₹ 59, 800

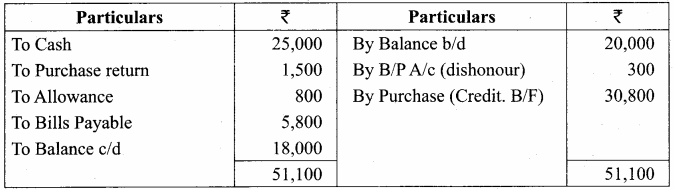

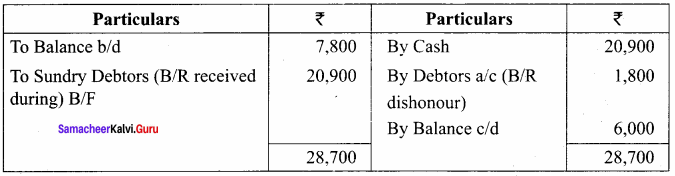

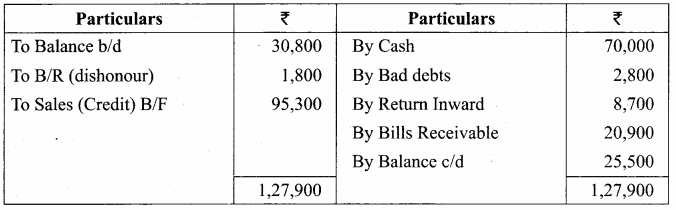

Question 6.

From the following information, you are required to calculate total sales.

Answer:

Bills Receivable Account

Total Debtors Account

Total Sales = Cash Sales + Credit Sales

= 40, 900 + 95, 300

= ₹ 1,36,200

Question 7.

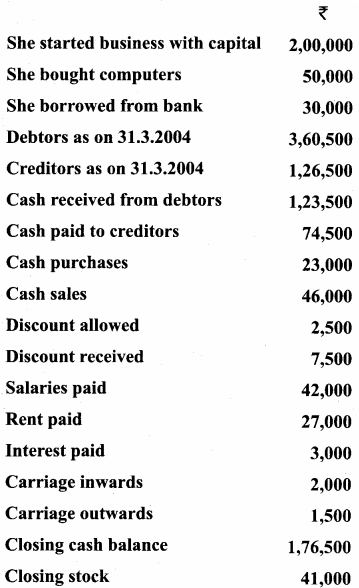

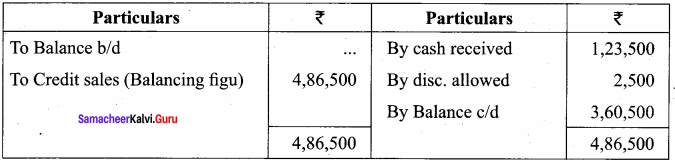

From the following particulars prepare the final accounts of Mrs. Meenakshi for the year ended 31.3.2004

Answer:

Total Debtors Account

Sundry Creditors Account

Question 8.

How to prepare the final accounts from incomplete records?

Answer:

When books of accounts are incomplete, information regarding revenues, expenses, assets and liabilities is not known fully. Hence it becomes difficult to prepare trading and profit and loss account and balance sheet.

Steps to be followed to prepare final accounts:

- The opening statement of affairs is to be prepared to ascertain the opening capital.

- Missing figures must be found out with the available date. This can be done by preparing memorandum accounts or by making necessary adjustments to the existing figure.

- It may become necessary to prepare a cash book to find out missing items such as cash purchase and sales.

- By preparing total debtors and total creditors A/c credit sales and credit purchases can be ascertained.

- Bills Receivable, Bills Payable A/cs are to be prepared to find out the balance of Bills Receivable. Bills Payable accepted.

- The final step is to prepare a trading and profit and loss A/c and balance sheet.

Question 9.

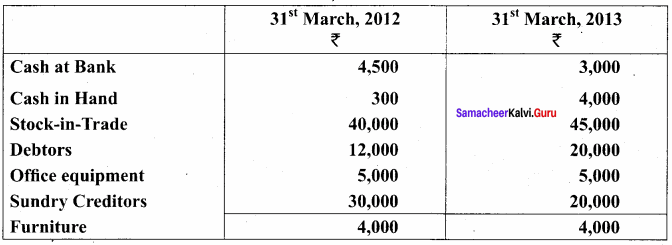

Kumaran, a trader does not keep proper books of account. However, he furnishes you the following particulars.

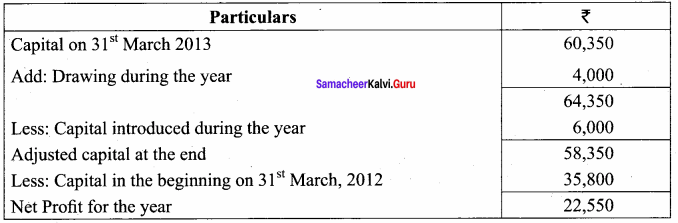

During the year Kumaran introduced Rs. 6,000 as further capital and withdrew Rs. 4,000 as drawings. Write off Depreciation on furniture at 10% and on office equipment at 5% Prepare a statement showing the profit or loss made by him for the year ended 31st March 2013.

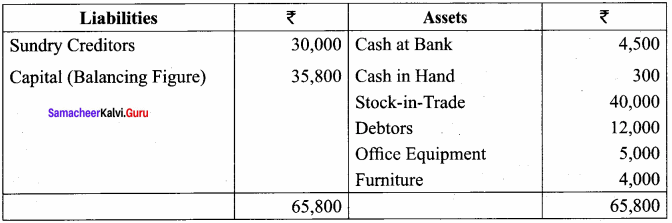

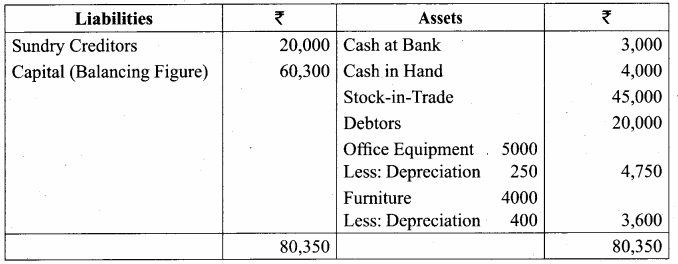

Answer:

Statement of Affairs as of 31st March 2012

Statement of Affairs as of 31st March 2013

Statement of Profit/Loss for the year ended 31st March 2013